< Back to all case studies

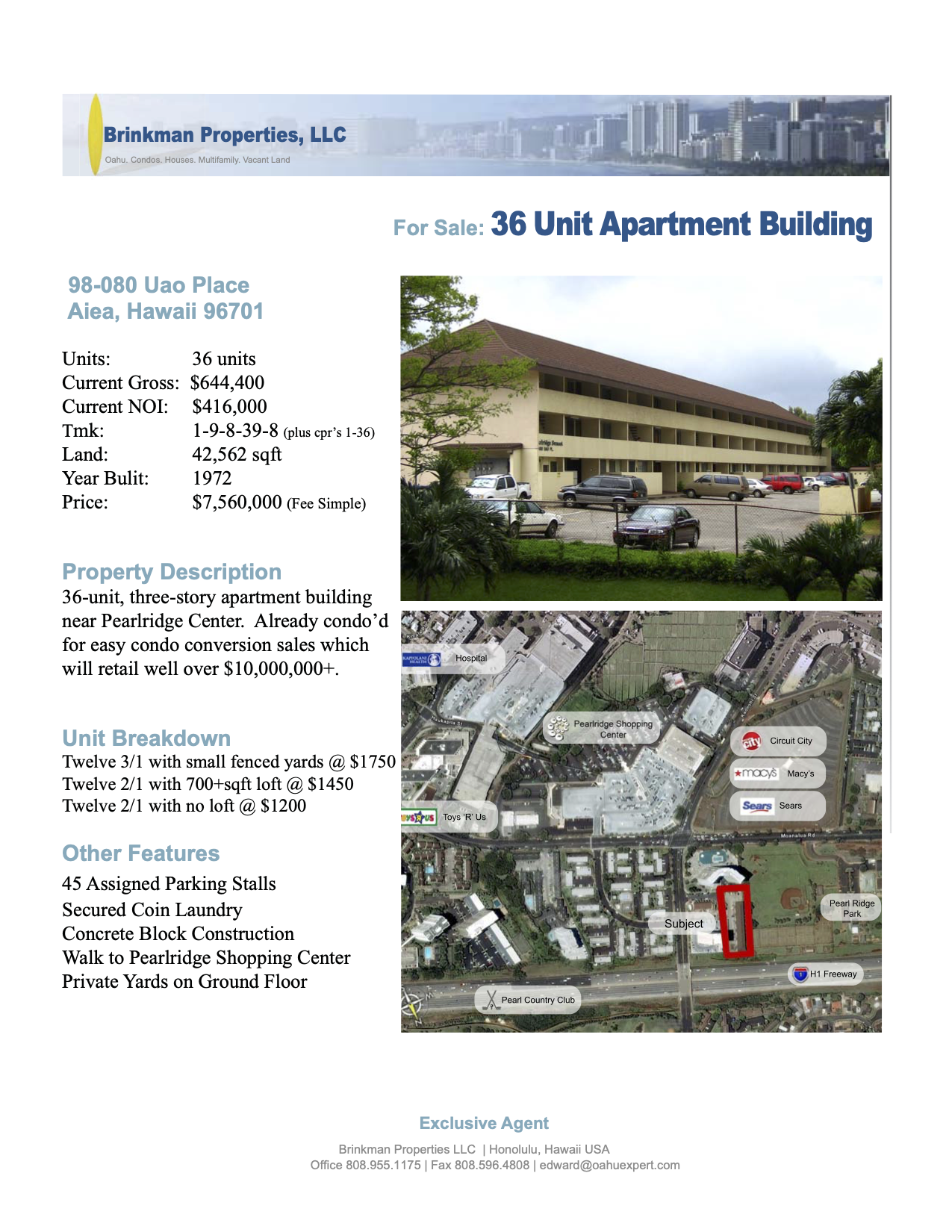

Purchase, Reposition and Sale of 36-unit Apartment Building

Client Buyer in 2005 for $5,750,000 and seller in 2006 for $7,750,000.

Assignment Buy apartment building at a low price and add value to sell at a higher price.

Challenges Adding value to the property to sell it at a higher price in a relatively short window of time.

Solution Put a condo map on the apartment building which would allow an investment buyer to buy the property based on condo values and sell them individually.

Result Sold the property to a local condo converter resulting in profits for both buyer and seller.